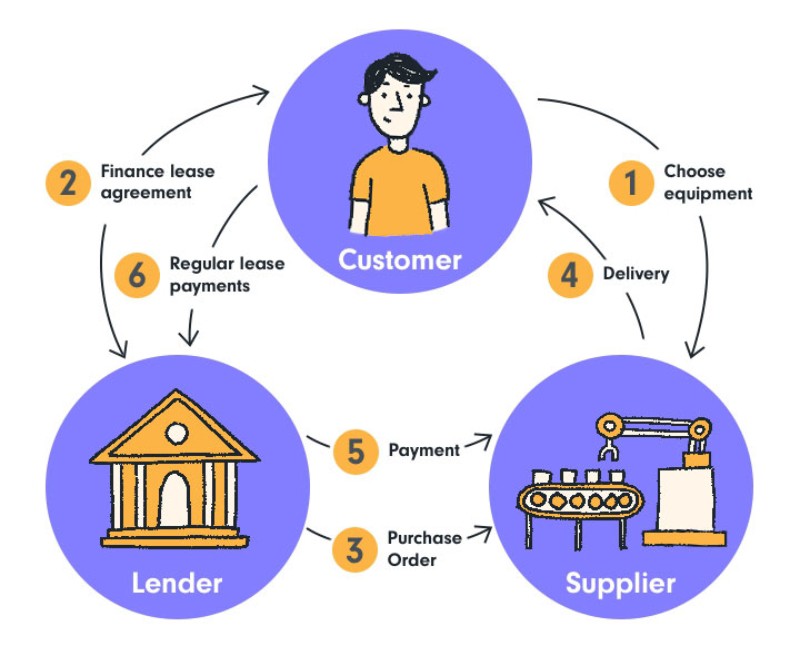

1. Basic tax treatment of lease and hire-purchase transactions:

The tax treatment of lease transactions in Kenya is based on whether the lease qualifies as a lease or will be treated as a hire-purchase transaction. If the transaction is treated as a lease, the lessor shall be eligible for depreciation on the asset. The entire lease rentals will be taxed as income of the lessor. The lessee, correspondingly, will not claim any depreciation and will be entitled to expense off the rentals.

If the transaction is a hire-purchase or conditional sale transaction, the hirer will be allowed to claim depreciation.

The financing charges inherent in hire instalments will be taxed as the hire-vendor’s income and allowed as the hirer’s expense.

2. What distinguishes between lease and hire-purchase:

Being the sole determinant of the tax treatment of leases, the distinction between lease and hire-purchase transactions becomes extremely important.

Essentially, the distinction is based on the beneficial ownership of the asset. In order to qualify for depreciation, the lessor has to establish himself to be both the legal and beneficial owner of the asset. As in a hire-purchase transaction, the lessor allows to the lessee the right to buy the asset at a nominal price, it can be seen that the lessor has parted with the whole of his beneficial interest in the asset. The lessor will not be able to benefit from the asset during the lease period (as there is a committed right to use to the hirer), and beyond the lease period (as there is a right to buy the asset with the hirer). Having thus permanently divested himself of his beneficial rights, the lessor becomes ineligible to claim depreciation.

As it is the beneficial ownership rights of the lessor that is crucial, the distinction between lease and hire-purchase goes beyond the mere existence of option to buy in the lease. If, explicitly or implicitly, it is apparent that the lessor has agreed to a permanent beneficial enjoyment of the asset by the lessee, the lease may be treated as a hire-purchase or a plain financing transaction.

3. Depreciation allowance on lease transactions:

A lease qualifying as true lease will entitle the lessor to claim depreciation. The true lease conditions and the conditions generally applicable for depreciation as such are not independent – the former are drawn essentially from the latter.

The tax-payer claiming depreciation should own the as

- (chars - 6985)

et. No doubt, the lessor owns the asset, but as discussed earlier, it is not legal ownership alone that is sufficient; the lessor must establish himself to be the beneficial owner as well. It is on the failure of the condition of beneficial ownership that the legal owner in case of hire-purchase is not allowed depreciation.

The lessor’s beneficial ownership of the leased asset is proved essentially by the right of reversion of the asset at the end of the lease period – this highlights the significance of proving that the lessor has a substantive and not merely notional or technical right of reversion of the asset

4. Rates of depreciation:

Rates of depreciation are listed in the Schedule to the Income-tax Rules.

Functional Test

Like under the English system, Kenya makes distinction between “plant or machinery” and other assets based on the functional test. The age-old functional test in Yarmouth v. France holds in Kenya. Based on this test, any assets that the lessor leases out are obviously income-earning tools in his business, and would therefore, be regarded as plant or machinery for his business.

5. Sale and leaseback transactions:

Sale and leaseback transactions came under a lot of flak during 1995-96, when transactions in junk funding were being labeled as sale and leasebacks at phenomenal values.

In some jurisdictions like India, the Income-tax law was amended to insert a specific provision about sale and leasebacks. It now restricts the amount to which depreciation can be claimed in a sale and leaseback transaction, to the written down value in the hands of the seller-lessee. That is, the actual cost of the asset to the lessor will be ignored, and instead, depreciation will be allowed on the seller’s depreciated value.

This provision is applicable only where the seller is the lessee; in other words, not applicable for every lease of second-hand assets.

6. Tax treatment in case of hire-purchase transactions:

In case of hire-purchase transactions, the hire-vendor pays tax on the income inherent in hire instalments, not on the whole of the hire rentals. Thus, the tax is charged only on the income, and not the inflow.

There are no well-defined rules on determination of income in case of hire-purchase transactions – therefore, accounting method adopted by the tax payer will generally be followed. Thus, either of the straight-line, sum-of-digits, or actuarial or IRR basis can be adopted for income allocation.

7. Deduction of rentals by the Lessee:

In general, in a lease, the lessee will be allowed to claim the rentals as an expense.

This is subject to general rules of reasonableness and the power of the tax officer to invoke substance of a transaction ignoring its legal form.

8. Depreciation claim by the Hirer:

The Legal Notice allows depreciation in case of hire-purchase to the hirer of the asset

9. Deduction of tax at source

Deduction of tax at source by the payer is applicable for several payments, including interest on loans.

There is no question of there being any loan or interest in case of lease transactions.

In case of hire-purchase transactions, a controversy was created recently in the context of Interest-tax Act. The resolution of the controversy seems to go into the vexatious question of substance of hire-purchase transactions.

10. Leases by cross-border lessors:

There is no major difference between leases by Kenyan lessors and cross-border lessors.

Kenya goes by the universal basis in computing and taxing income – therefore, income deemed to accrue and arise in Kenya, even for entities not resident in Kenya, will be taxable here. Income arising out of an asset in Kenya will be deemed to accrue and arise in Kenya. Hence, in a lease, or in a hire-purchase transaction, the hire rentals, will be deemed to accrue or arise in Kenya if the either the asset or the tax-payer is do